The percentage of GDP that the state spends on pharmaceuticals has not increased in the last 20 years.

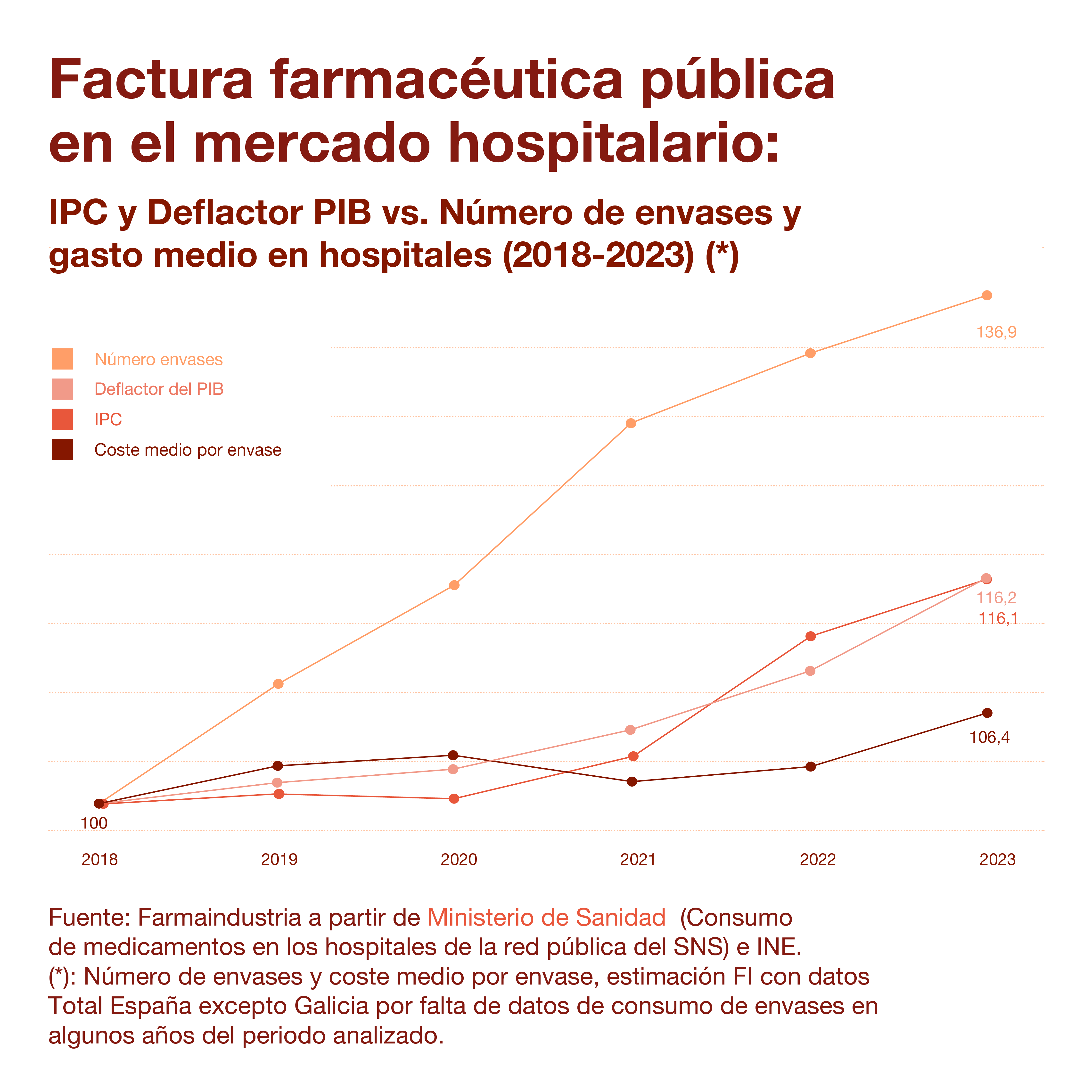

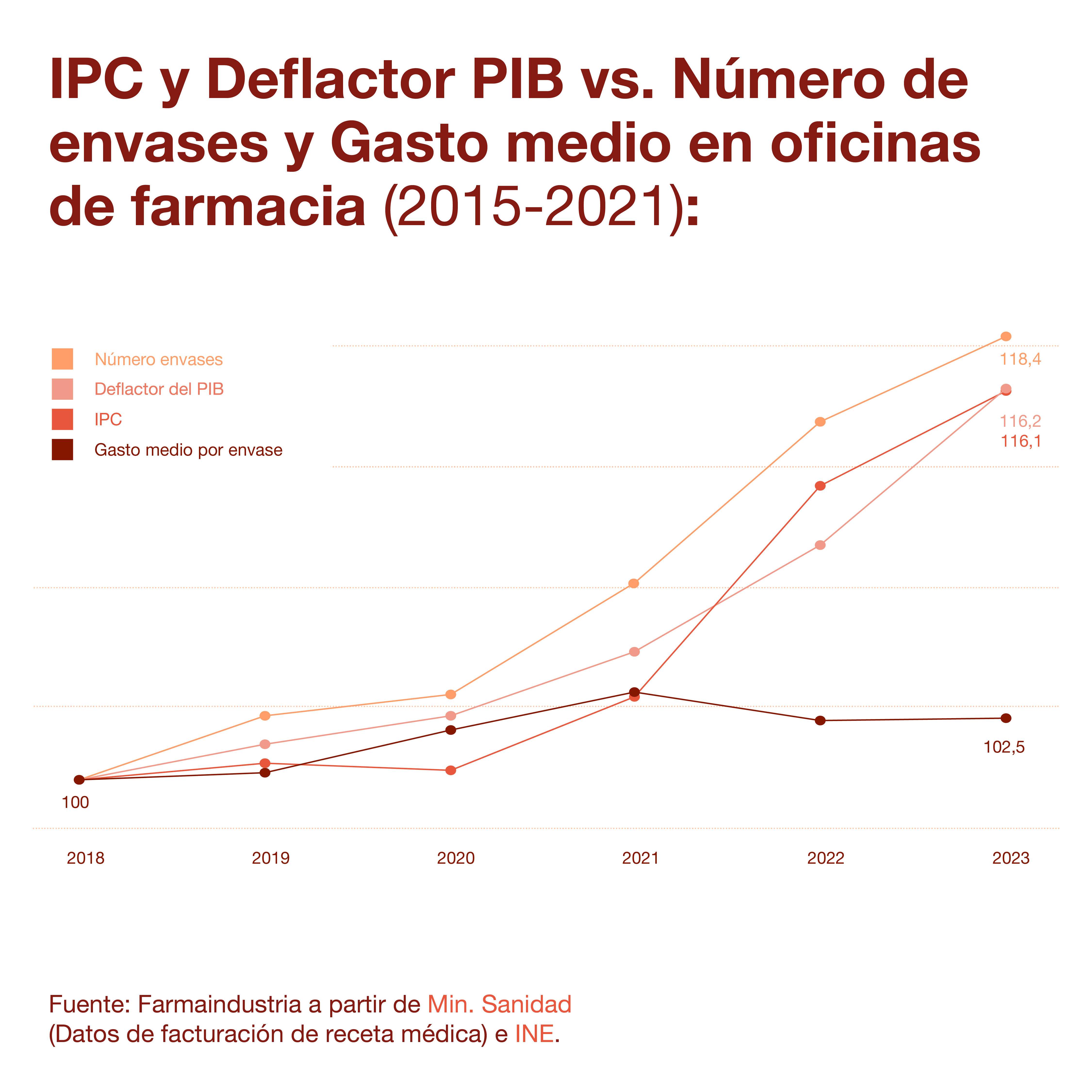

Between 2018 and 2023, the increase in the average price of medicines has been 6.5 times lower than inflation in pharmacies and 2.5 times lower in hospitals.

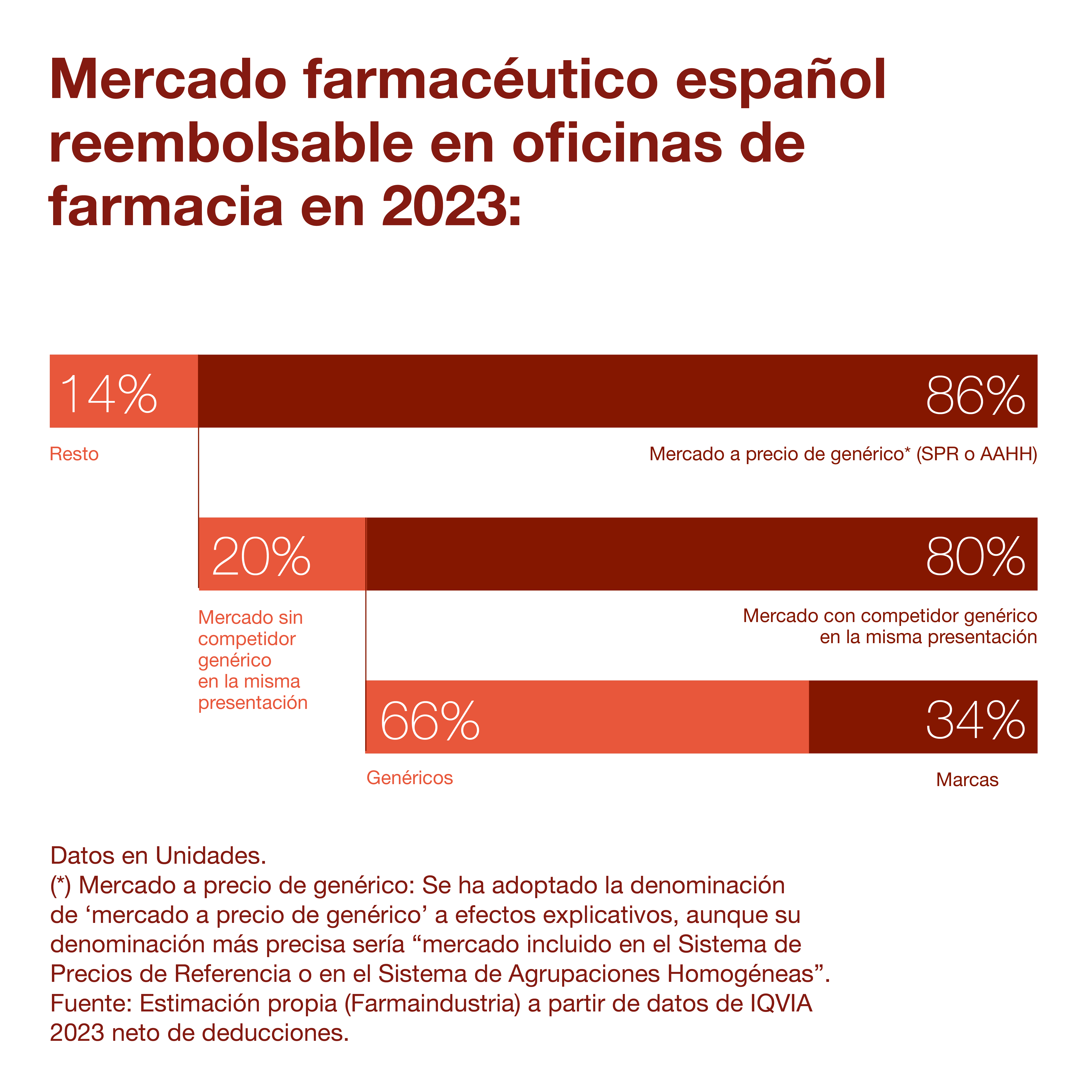

86% of the units of medicines sold in pharmacies (branded and generic) are at generic prices, and in the market segment where generics choose to compete, generics have a 66% market share.

Farmaindustria.es

The recent report The pharmaceutical industry and its context in Spain 2024 gathers the main data on the pharmaceutical market in Spain and frames it in terms of its impact on the National Health System, taking into account its evolution over the last few decades.

The following are some of the key aspects of this issue.

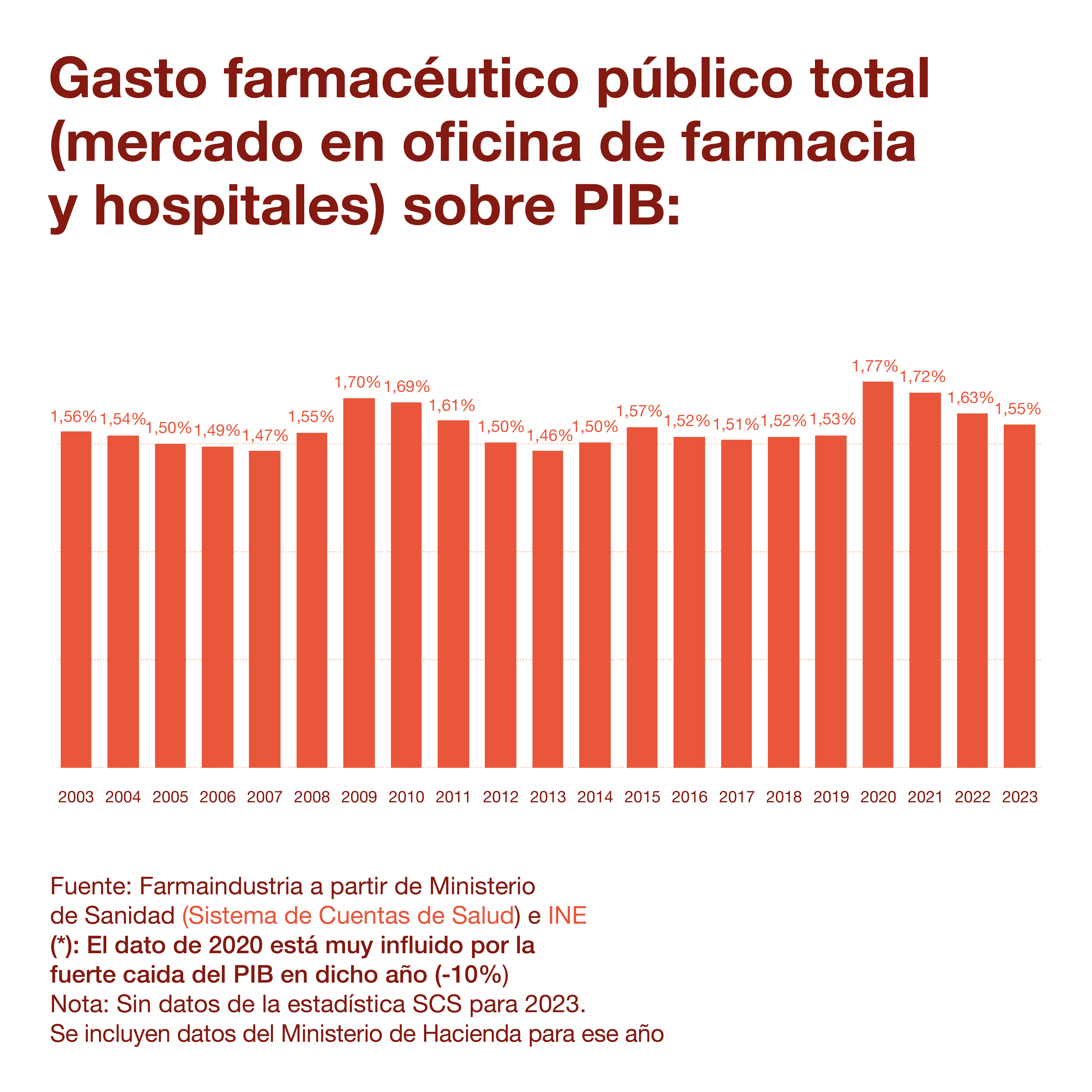

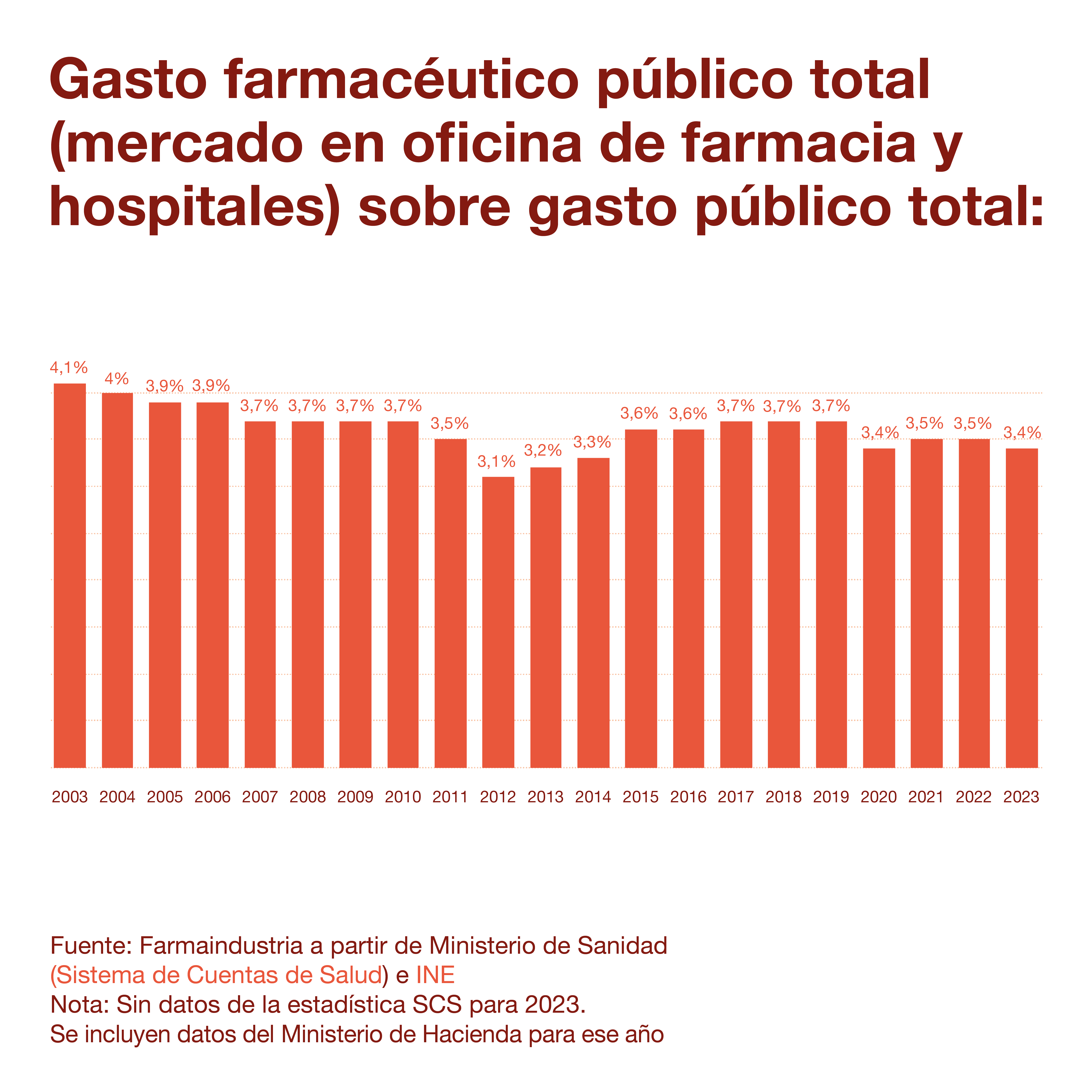

Stability of public investment in medicines

Public investment in medicines has remained stable historically. As can be seen below, the percentage of GDP represented by government investment in drugs has not increased over the last 20 years, with the exception of cyclical situations caused by economic shocks; the same is true when compared with total public spending, where a downward trend can be seen in the long series.

Farmaindustria.es

Farmaindustria.es

These data shown in the graphs reflect the idea of long-term economic and financial sustainability of public investment in medicines.

1.1. Inflation much higher than the increase in average medicine prices

In fact, in recent years, the increase in inflation has been much higher than the increase in the average price of medicines, both in the hospital market and in pharmacies.

In the case of medicines dispensed in hospitals, while the CPI has risen by 16.2% in the five-year period 2018-2023, the average price per hospital pack has risen by 6.4% in the same period. In other words, the price of medicines has increased 2.5 times less than inflation in Spain.

Farmaindustria.es

In the case of medicines dispensed in pharmacies, in the five-year period 2018-2023, the average expenditure per pack has risen by 2.5%. Compared to the 16.2% increase in the CPI, the increase in the average price of medicines dispensed in pharmacies in Spain has been 6.5 times lower.

Farmaindustria.es

It should also be noted that the increase in public spending in recent years is mainly due (more than 80%) to the increase in the volume of purchases. This is due to various factors: the main ones are ageing and the increase in chronicity, but there is also an increase in the population, in the incidence of certain diseases and the increase in activity resulting from preventive policies, such as screening for certain diseases, which increase health and pharmaceutical spending in the short term, but generate savings in the medium and long term thanks to the prevention or early treatment of pathologies.

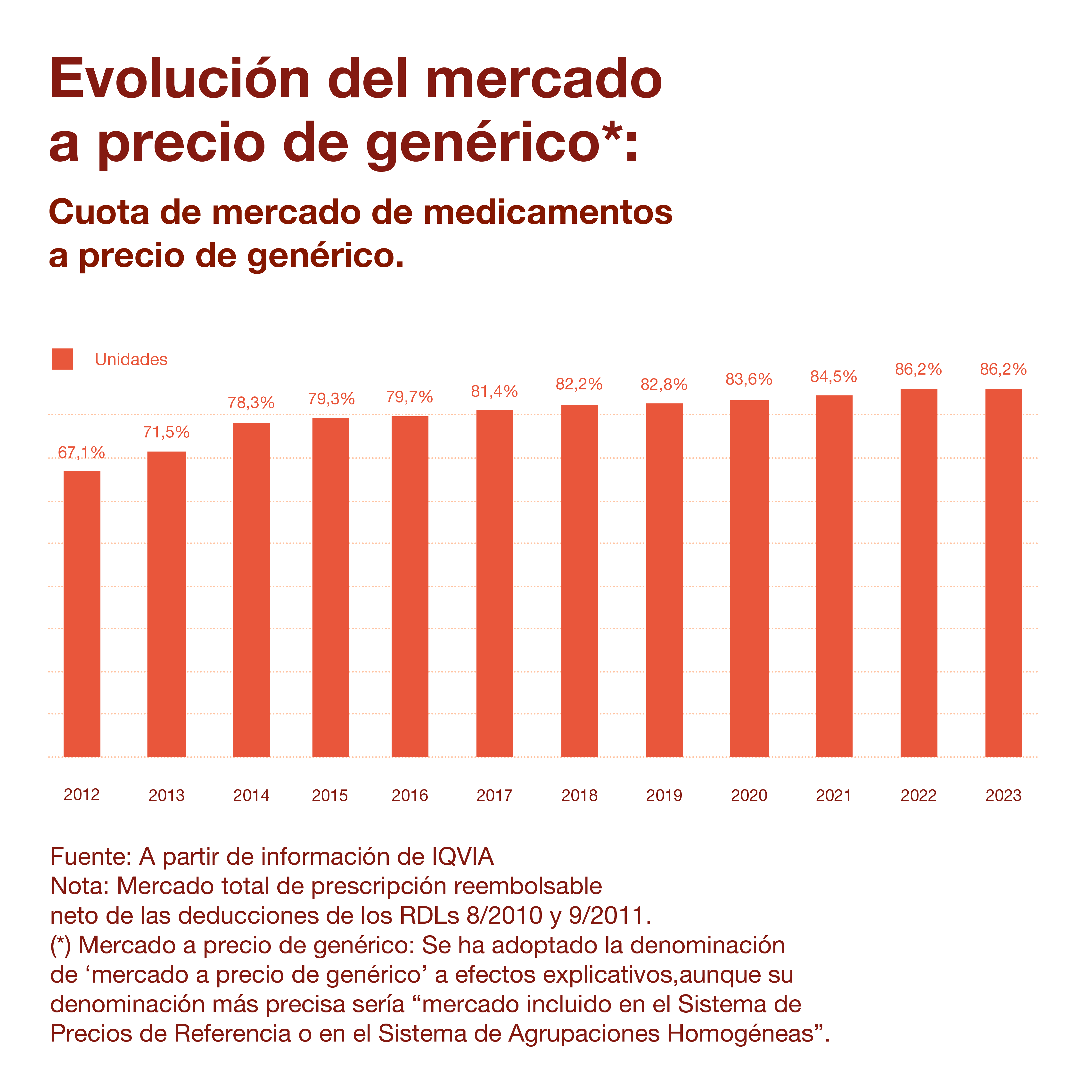

2. The pharmaceutical market at generic prices is on the rise.

Of the Spanish pharmaceutical market subject to public reimbursement in pharmacies, 86% of the units dispensed are affected by the Reference Price System or Homogeneous Groupings (SPR or AAHH), which include medicines that have lost their patent. The remaining 14% are medicines that are still under industrial property protection.

As the graph below shows, the percentage of medicines at generic prices has grown significantly in the last decade (it was 67.1% in 2012).

Farmaindustria.es

Of this market affected by the SPR or AAHH, 53% of the units correspond to generic medicines and the remaining 47% to non-generic medicines, including mainly branded medicines at generic prices, which contribute in the same way as their generic equivalents to generating savings for the National Health System.

However, in this medicines market affected by the SPR or AAHH, 80% of the units dispensed correspond to presentations where there is direct competition between original medicines and their corresponding generics. The remaining 20% of presentations have no generics on sale, with only branded presentations. This is, in many cases, due to the lack of commercial interest of generic companies in low-dose, paediatric or other medicines.

Of this segment that has original and generic medicines in the same presentations, generics have a unit market share of 66%. In other words, in those presentations of medicines where originator and generic medicines compete, two out of every three units sold are generic and one is a branded medicine.

Farmaindustria.es

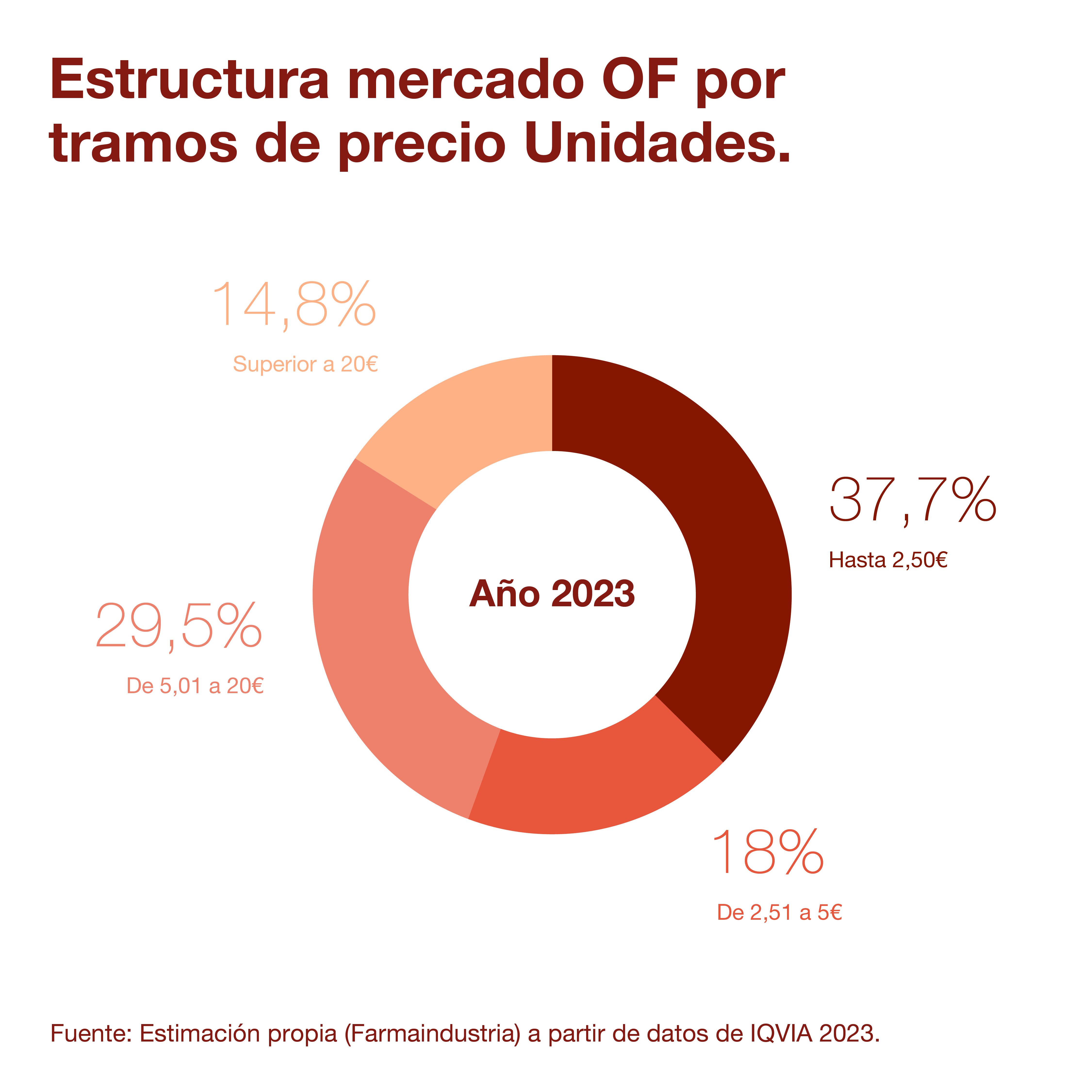

3. More than half of the medicines, at less than five euros

Currently, almost 40% of prescription medicines dispensed in pharmacies cost less than 2.5 euros and more than half (56%) cost less than 5 euros at RRP including VAT.

It should be remembered that, once generics enter the market, these and branded medicines are at the same price and generate the same savings for the NHS.

Farmaindustria.es